%20(1).webp)

It is particularly interesting that US Treasury Secretary Bessent is in Tokyo today (12 May) and tomorrow (13 May) to undertake separate meetings with PM Takaichi, FinMin Katayama, and BOJ Governor Ueda, before joining President Trump's summit meetings in China from Thursday (14 May). While the China Summit, the Iran conflict and other geopolitical matters are no doubt on the agenda, it is believed that Bessent's primary focus here will be on Japan's economy and markets – particularly on the weakness of JPY. The timing is pivotal, coming only days after BOJ's 28 April Outlook Report sharply raised its inflation forecasts, the govt's yen-buying intervention only 2 days later, and only a few weeks ahead of a now-widely-anticipated BOJ rate hike at its next (15-16 June) Board meeting.

Readers of my last two Insight notes – "The BOJ tries going full Hawk …" (28 Apr 2026), and "So JPY broke the 160 red line…" (1 May 2026) – written on the BOJ's hawkish turn and the MoF's subsequent JPY intervention, will understand that it usually requires both repeated interventions and a monetary policy change for interventions to work. Credibility is key, which is surely a consideration behind Bessent's visit. But that it is Bessent himself undertaking these meetings - alone - adds another layer of significance that turns his visit potentially into a pivotal macro catalyst – and not just for JPY.

This is because Bessent – an expert on the whole BOJ–JPY–JGB nexus from his macro trader days – has been voicing surprisingly-public warnings on Japan for many months now. Recall in August last year, he openly suggested the BOJ was "behind the curve" and "need to get their inflation problem under control" - a comment that BOJ Gov Ueda sternly rejected at the time (which will make for an interesting backdrop to their meeting this week, as it was Bessent who was arguably more correct). Then in October too, during his last visit, Bessent pointedly reminded the newly-minted PM Takaichi that her "willingness to allow the Bank of Japan policy space will be key to anchoring inflation expectations". And most tellingly, the Nikkei revealed only last week - something not previously in the public record – that on 23 January this year, it was Bessent who personally initiated the US Treasury Dept's "rate check" when USDJPY threatened the 160 level. At the time, it was assumed to be the BOJ (under instruction from the MoF) that undertook the rate check. That it was Bessent's call, strongly suggests the 160 level is not just the MoF's "red line" – but his too. Maybe it was always his call. There's the credibility FX markets may have been looking for.

Could this then be the trigger for a more sustained reversal in USDJPY?

So, based on the above, Bessent's meetings today and tomorrow may serve to enshrine the USDJPY 160 "red line". But could it go much further – and be the catalyst for a more sustained reversal in USDJPY?

Late last year, I wrote an Insight post - "Could the yen snap back?" (12 December 2025) that showed that while a weakening JPY looked to many like a one-way secular trend – beneath the surface, there remained a structurally-embedded reversal risk, driven by Japanese residents' own outward portfolio flows, the colossal stock of overseas assets they had built up, and the policy-convergence and domestic-shock channels that could turn that flow back.

While a "yen snap back" is still very non-consensus, it is interesting how an increasing number of reputable players have also voiced this view. In a podcast interview from mid February (that went somewhat viral after been published in late April), legendary macro trader - Paul Tudor Jones – put a JPY strengthening turnaround as one of his highest-conviction trades for 2026. He described the yen as "grossly undervalued," citing the same underlying portfolio positioning that I did, saying; "Japan has a $4.5 trillion net international investment position to the good with the rest of the world, probably 60% of that's in the US. And most of that is unhedged. So they just had this massive dollar liability."

From my December Insight; "The magnitude of these resident outflows - and the latent potential for repatriation - should not be underestimated. Japan's net international investment position remains one of the largest in the world, with overseas assets held by Japanese residents exceeding ¥500 trillion. This colossal stock of foreign assets means that even small shifts in repatriation behavior can translate into outsized yen demand. Were households or institutions to start reducing foreign exposures or hedges, the scale of currency turnover could be large enough to produce a meaningful snapback in JPY. The key point is that this latent pool exists precisely because the current flows have been one-directional; once sentiment shifts, the same structural channels that facilitated outflows can work in reverse."

Others too have picked up on these points. Another legendary macro trader, Stan Druckenmiller, expressed something similar, noting around the same time as PTJ did, that; "foreigners are way, way overloaded in dollars," with disclosed "big positions in Japan and Korea." And of course Scott Bessent himself shares a similar legendary status – especially with regard to Japan macro trades – and one imagines he also shares these views.

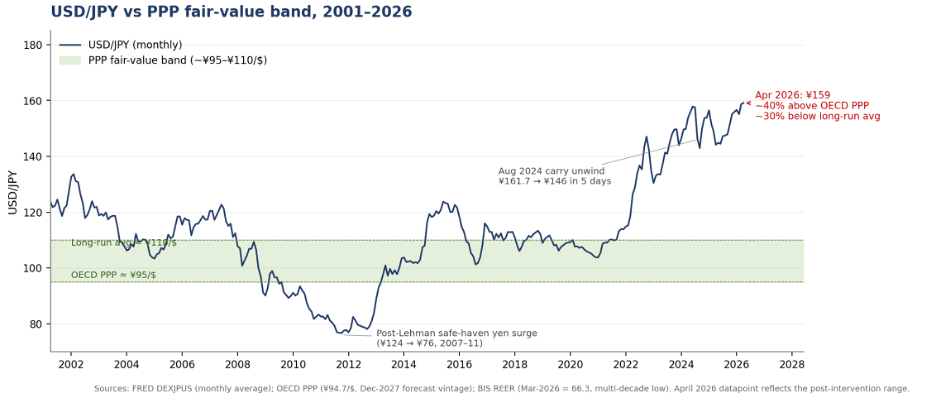

And it's not just positioning. On valuation too, JPY has rarely been this far from "fair value

"While calculating a currency's "fair value" using PPP or other such academic measures of "real" exchange rates is often of little relevance to actual FX levels – it is worth noting, in the above context, that most of the standard measures of the yen's "fair value" are currently at an extreme. The OECD's PPP of USDJPY is around ¥95 - a near 40% undervaluation (see the chart below). The Economist's Big Mac Index has Japan 50% undervalued in 2026, a record post-1986 while the BIS broad real effective exchange rate for the yen (FRED RBJPBIS, March 2026) is at 66.3, its lowest level since the index began in 1964. Even when acknowledging that JPY is rarely ever aligned with such structural measures, it is hard to ignore just how historically extreme its current misalignment is. Mean reversion alone, without any new catalyst, has produced moves of 15%-plus from this configuration in the past.

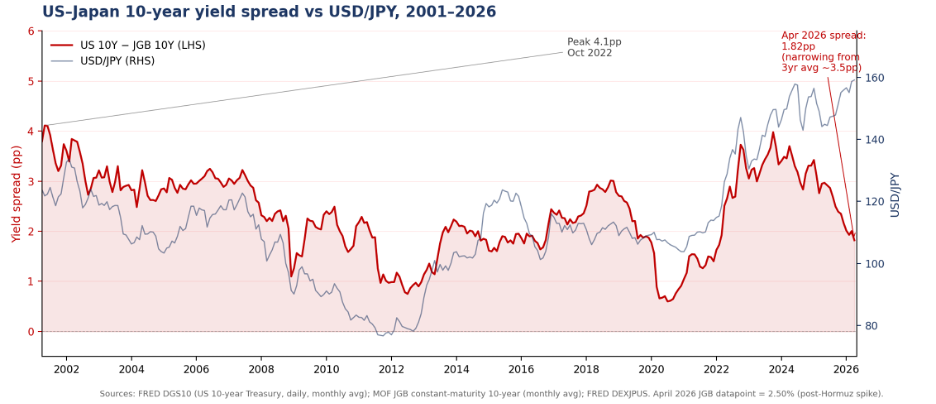

And even the UST-JGB yield differential now points to JPY strength

A much better predictor of USDJPY than obscure "fair value" measures, has been the UST-JGB yields differential. The chart below shows how closely USDJPY has tracked the UST-JGB 10-year spread through this cycle. But it also shows now how even that relationship has started to decouple – with the spread compressing sharply in the last year or so, even as USDJPY has continued to rise. A June BOJ hike would cut the spread even further – as of course would a Fed cut too. Both seem real possibilities – especially the BOJ hike (in the context of Bessent's visit).

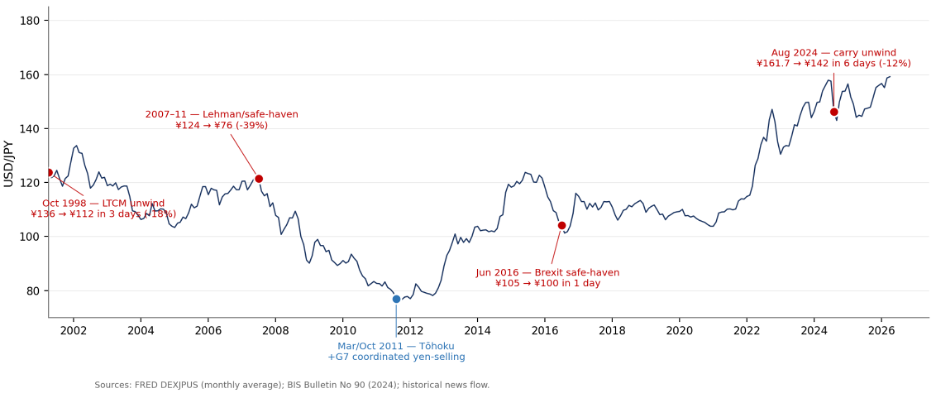

Historical analogues — what a USDJPY snap back may look like

History shows that JPY snap-backs often occur and can be sharp. The chart below shows that sudden moves of around 10-20% in only days are not uncommon – and can be even larger. The most recent such move was the carry unwind from 5 August 2024 – whereby the BOJ's late-July 0.10%→0.25% hike and a soft US July payrolls print, triggered JPY to jump 12% in six trading days (from ¥161.7 to ¥142), while the Nikkei fell 12% in a single session (and even the S&P came off 3%). The October 1998 LTCM unwind was sharper still – an 18% move (from ¥136 to ¥111) in just 3 days. If similar moves were to happen now, it would imply a quick test of the ¥140 area, or even ¥130. Neither such move is in any consensus. And I doubt that even Paul Tudor Jones is thinking that – but it's easy to imagine he too sees that possibility.

So, beware the snap-back risk – and also its broader risk-appetite tail

Summing the above points – across positioning, fair valuation, yield differentials and policy timing – it's easy to see how USDJPY may be particularly vulnerable to a snap-back - and how Bessent's current visit to Japan could help trigger it. But it's probably fair to say that Bessent himself sees it too - and so may be cautious not to trigger it. For while Bessent may favour a stronger JPY and a higher BOJ policy rates, he is unlikely to want the follow on effects that may come from that. The August 2024 snap-back offers a reminder of what an unhedged-NIIP unwind can do for global risk appetite, if only briefly. A sudden but sustained turn to JPY strength would reflect an unwind of the world's largest unhedged carry book. So, played badly, such a snap-back could ultimately transmit as a global risk-off. The next few days and weeks will tell.

.svg)