.png)

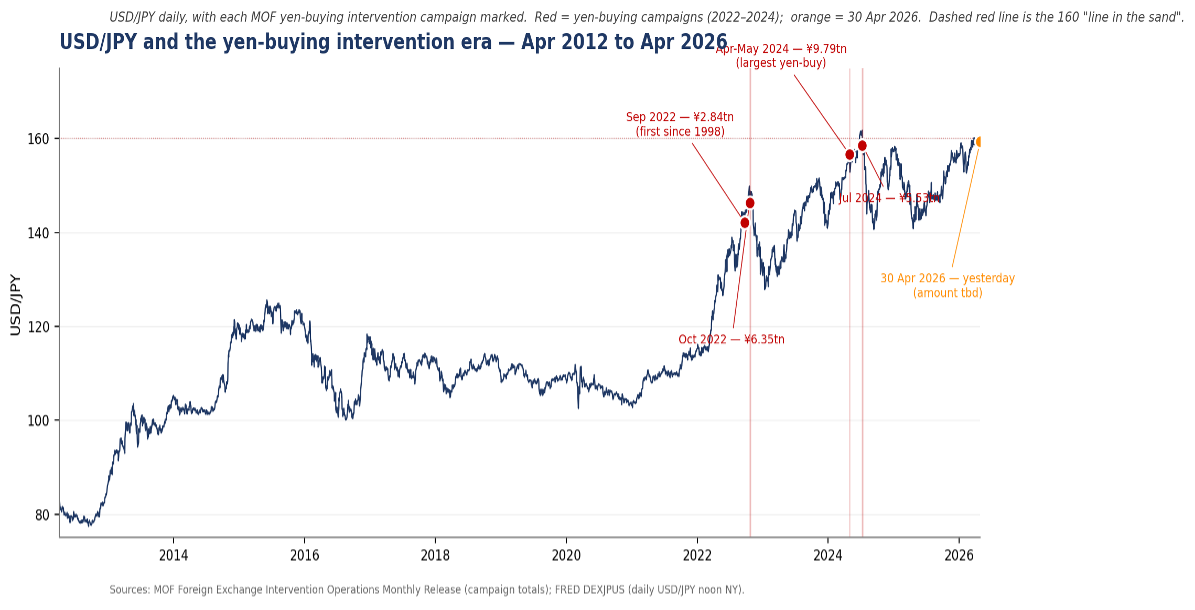

Last Tuesday, I wondered whether the BOJ's sharp hawkish pivot in its April Outlook Report was enough to hold USDJPY at the 160 "line in the sand" – especially through Golden Week ("The BOJ tries going full Hawk – But will it hold JPY at 160?"). It didn't take long to get the answer. USDJPY held valiantly just below the level for a couple of days – but made a successful push through it on Wednesday, the first official day of Golden Week. This prompted the usual verbiage from the FinMin Katayama, followed by actual JPY-buying intervention by the Ministry of Finance (MoF) on Thursday – pushing USDJPY back to the 155 range. As Japan enters the main block of Golden Week, a no-doubt nervous Katayama warned observers to "carry your smartphone close at all times including during the holidays." So begins a familiar waltz between the Government and FX markets – but which is, ultimately, more crucially between the Government and the BOJ.

First, a piece of housekeeping that matters more than the press shorthand suggests. In Japan the authority to instruct an FX intervention sits with the MoF – and so the decision is the FinMin's. Despite the BOJ clearly trying to stem the JPY's fall earlier this week with its hawkish turn, when interventions occur, the BOJ is only the executing agent. So, when news wires call this a "BOJ intervention" they leave the wrong impression. It was Katayama's call – not Ueda's – and that clarification has implications

Thursday's yen-buying intervention is now the fifth time the government has done so since September 2022. While interventions had occurred over the previous decades – mainly in the period from 2001 to 2011 - 2022 marked the first time in 25 years that the interventions turned consistently to yen-BUYING – a reflection of the gradual emergence at that time from a generation of deflation.

But in 2026, that gradual emergence has now switched to full-on inflation. And as the BOJ's Outlook Report noted on Tuesday, the "risks to prices are skewed to the upside". Clearly, the rate of this switch is surprising policymakers. And I suspect, it's beginning to scare them too.

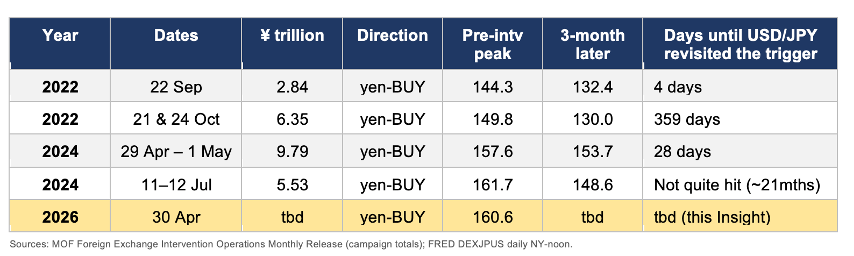

The pattern of interventions – especially those since 2022 - suggests it takes more than one strike to stem the pressure, and that it is not long before market selling pressure resumes. The table below sets out for each yen-buying campaign the pre-intervention peak that triggered the action, the spot rate roughly three months later, and the number of days before the FX market revisited that trigger level. The first strike of an intervention pair almost always fades quickly: the September 2022 ¥2.84 trillion campaign was unwound in four days; the April-May 2024 record ¥9.79 trillion campaign - the largest yen-buying campaign in history - was unwound in 28 days. It is the second strike that does the work. October 2022's ¥6.35 trillion held the line for almost a year. July 2024's ¥5.53 trillion has held for nearly two years and counting.

The reason both "successful" follow-ups stuck was not size - they were each smaller than the campaign that preceded them - but timing. Both arrived alongside a parallel turn in monetary policy. October 2022 came as the Fed's hiking pace was about to slow; July 2024 came in the very week the BOJ delivered its pivotal hike from 0.10% to 0.25% on 31 July, with further hikes to 0.50% in January 2025 and 0.75% in December 2025 to follow. Without a parallel policy shift, interventions tend to smooth but not hold. The implications for another yen-buying intervention soon, and for rate hike at the next BOJ meeting (June 15-16) seem clear.

First, the very fact that the MoF acted on the eve of Golden Week - with local traders on vacation for almost a week – underpins the BOJ's earlier hawkish signal. That timing, plus the rhetoric, strongly suggests that Katayama understands that a follow-up hit is likely - if even inevitable – and could be required in a matter of days.

Second, the historical record of interventions also supports that pattern.

Third, and most important for FX markets; yesterday's intervention clearly marks out the 160 level as a clear "red line" for the government. And that poses a dilemma for the government. For history suggests that whether that "red line" now holds depends not on the size of the next intervention but on whether the BOJ also delivers on the hawkish forecast set it published on Tuesday.

And here is where the dilemma sharpens - particularly for PM herself. Takaichi has spent the better part of two years publicly arguing for a dovish BOJ: in September 2024 after calling the BOJ's rate hikes "foolish (あほ)", she said "the government must take responsibility for both fiscal and monetary policy", and in February this year she reportedly conveyed direct reluctance over additional hikes to Governor Ueda. And to top it off, in that same month, she nominated two known doves to the BOJ Board.

So, if the historical pattern holds, such that the price of holding the 160 "red line" is now a BOJ June hike, Takaichi may find herself having to advocate the very policy stance she has hitherto argued against. That is, if she really intends to hold the 160 line. Given the circumstances, she may not.

Either way, unless there is a significant and sustained retreat in USDJPY now – and recent history and context suggests otherwise – the Japanese government finds itself in quite a pickle. For those in Japan – enjoy your Golden Week. But, as FinMin Katayama says, "carry your smartphone close".

.svg)