.webp)

On the eve of Japan's Golden Week, with NKY225 punching through a record 60,000 and USD/JPY again pressuring 160 –a level the MoF has set as a line-in-the-sand - today’s BOJ board meeting and April Outlook report was a pivotal test. A delicate balance could break if they’re not careful.

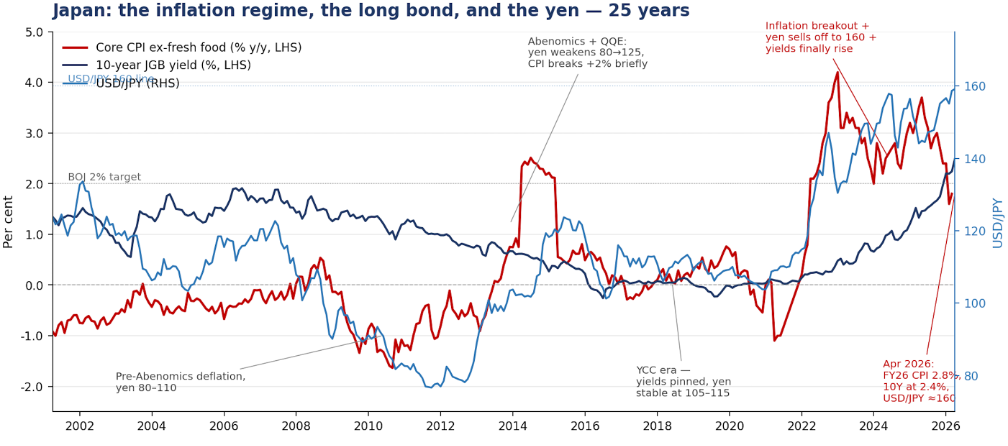

As widely expected ahead of the meeting, the Board chose not to raise rates this time – but it seems to have done everything else to it could to signal that it probably should have – and most likely will do so at the next (June 15-16) meeting. There were three dissenters (out of 9) who wanted to hike. In the way these go, a fourth dissenter would’ve risked making the Board looked confused or in conflict. But three makes it look like it wants to just give everyone a month’s warning. This is backed up too by the Outlook Report – with it updated CPI forecasts jumping for this year and next; Median CPI from+1.9% to +2.8 in FY2026 (Core CPI from +2.2% to +2.6) – and from +2.0% to +2.3 in FY2027 (Core CPI from +2.1% to +2.6). This are huge increases vs the previous forecasts (made in only January) – and to well above the 2% core CPI target.

Moreover, in addition to the magnitude of the inflation forecasts revision, the report also changed its assessment of the balance of risks to "risks to prices are skewed to the upside, while risks to economic activity are skewed to the downside." This is not just significant because it follows fifteen months in which prices were assessed as either skewed to the downside or generally balanced, but also because the balance they are describing is stagflation.

Finally, in the “Conduct of Monetary Policy” section, that hikes are coming soon is explicit: "given that underlying CPI inflation has been approaching 2 per cent and real interest rates are at significantly low levels, the Bank will continue to raise the policy interest rate,”. The only variable is given as “the future course of the situation in the Middle East.”

The signalis clear. Prepare for rate hikes.

So why the tough talk now?

As I have laid out in a couple of previous Insights - "Do the Japanese have an inflation problem? Understanding Bessent's concerns" (10November 2025) - and more pointedly in; "A record budget, a surging yield curve, inflation and now… a war" (7 April 2026) – Japan’s emergent inflation is at risk of being dangerously amplified by multiple concurrent factors, including; the sharp shift from a deep deflationary mindset forcing a sudden portfolio rebal; aggressive reflationary fiscal policy; a persistently falling currency; and exploding (but subsidized) energy prices - and, importantly, a monetary policy that is widely perceived to be permanently ‘behind the curve”.

The implicit concern – although one that is becoming increasingly explicit - is that this will see the hitherto orderly process of interest rate normalization turn disorderly. The recent rise in long bond yields and a USD/JPY pushing repeatedly up against the Y160 “line in the sand” is fueling such concerns. Today it would seem the BOJ board has decided the time for tough talk has come.

Is the BOJ now trying to get infront of the curve?

On this, I recall that when Treasury Secretary Bessent controversially warned that the BOJ was "behind the curve" (in August last year), BoJ Governor Ueda sternly rejected the accusation. But today’s Outlook Report, in narrative terms, is almost an admission now that Bessent was right, with it forecasts ratifying the very dynamics Bessent flagged - sticky underlying inflation, firms shifting more decisively toward raising wages and prices, an output gap in positive territory, and inflation expectations rising. Indeed, every one of the seven inflation factors my November Insight note set out is now reflected in theBOJ's own report.

But what if it doesn’t work?

At least in the few hours since the BOJ’s meeting and the Outlook Report, USD/JPY has held the 160 line – but only just – and not enough perhaps to give comfort to the board that its hawkish turn has credibly put the BOJ in line. With Japan now about to enter its traditional Golden Week holiday, and most of the other amplifying factors discussed above still just as much in playas before, I suspect a break higher than 160 in USD/JPY is coming soon. And then what can the BOJ do? Realistically, how could they be much more hawkish than they were today?

.svg)