.webp)

Allocators' reflex to the "Japan is Changing" pitch

As anyone who's studied for the CFA knows, the definition of beta is "the return attributable to holding the market portfolio" - the return you earn simply from being exposed to a broad market or risk factor. Alpha, by contrast, is the residual: the portion of return that cannot be explained by market exposure. As Michael Jensen formalised it in 1968, alpha is the measure of a manager's ability to generate returns above what the market, adjusted for risk, would predict. And as William Sharpe famously refined it in his celebrated 1991 essay The Arithmetic of Active Management; before costs, the average actively managed dollar must equal the return of the average passively managed dollar. That is, if you can get the return from an index fund, why are you paying a manager? The implication: to justify active fees, a manager must demonstrate genuine alpha - returns that cannot be replicated by simply buying the index.

This framework has become the catechism of institutional asset allocation. And yet it poses a very specific problem for anyone trying to explain the massive investment opportunity still playing out in Japan today.

The beta or alpha question for Japan-focused funds

When a Japan-focused fund sits down with a global allocator and says: "Japan is undergoing a generational transformation - three decades of deflation are ending, demographics are forcing corporate reinvention, governance is being overhauled, and a new cohort of leaders is rewriting the rules," the allocator hears something very specific. They hear macro. They hear thematic. They hear beta.

And they switch off. Because if the entire thesis is "Japan is changing," that sounds like a country bet - a view on a broad market risk factor. And a country bet is beta. And beta can be acquired for 5 basis points via an ETF. So why pay for active management?

The very scale and breadth of what is happening in Japan - the fact that it touches everything, from wages to capital allocation to corporate identity - makes it sound, in the language of portfolio theory, like beta. But that classification is a profound misunderstanding. And it could be costing allocators access to one of the richest alpha-generating environments seen in global equity markets in decades.

The Reframe: Market-Wide Phenomena, Company-Specific Impacts

Consider the end of deflation. Yes, it is a macro phenomenon. Yes, it is economy-wide. But what happens at the company level when a thirty-year deflationary trap mindset finally breaks? Some companies - those led by a new generation, those already investing in pricing power, those restructuring their cost bases - recognise the shift early. They reprice their products. They take on productive leverage for the first time in decades. They invest in capacity and talent. They "use their cash" (before they lose it). Such companies can now compound value at a rate that was structurally impossible under deflation.

Others (and there are many) - still run by aged-leaders forged in the deflationary era, still hoarding cash, still cutting prices to defend share, still refusing to hire mid-career talent - are falling behind, and will continue to do so. Not gradually, but decisively. Because the environment that protected them for so long has gone.

Buying the former and shorting the latter is not riding a wave, nor is it a country bet. It requires careful, studied stock selection by expert asset managers - informed by a structural view, but identified and executed at the individual security level. That is alpha.

The once-in-a-generation structural phenomena provide the context in which the alpha is extracted by identifying how individual Japanese companies are able to deal with these new conditions - to see which of them are on the right side of the shifts and which are not. And this logic applies not just to Japan's seismic demographic shifts or the end of 3-decade deflation, but to the myriad other derivative – and huge alpha-generating - phenomena currently underway in Japan.

Understanding the Two Core Structural Shifts – 1) Demographics and 2) the End of Deflation

But before exploring those derivative phenomena, it is worth reflecting on just how seismic the core two shifts underpinning the alpha-opportunity in Japan are. These are: 1) demographic change; and 2) the end of deflation.

Japan's demographic changes: The most-stark generational change in the World – Forcing multiple transitions and transfers, including importantly in decision-making power.

As I wrote in my first ever "Insight" post for GBM AM the disruption of WW2 and no subsequent immigration saw Japan's demographics become the most starkly delineated and consequential of any country in the world. Its post-war age pyramid became distinguished by two distinct humps - the first reflecting an explosive baby boom in the immediate post-war years (~1946-50) – and the second reflecting when those "boomers" all had kids ("juniors") of their own (~1970-75). Not only is it that these two generational humps are so distinct, but more importantly, that the life experiences of those within each hump is so different from each other. And that difference is crucial to understanding how demographics is driving change in Japan right now - across all levels of society, but particularly to company managements, public policy formation and household financial portfolios – all in themselves offering massive opportunities for extracting alpha.

And that doesn't even address the most commonly-cited – and frankly least-interesting – fact about Japan's demographics - which is that the population is rapidly shrinking and aging at a rate now that is seeing its working-age population decline by more than a million people a year. It's not rocket science – nor indeed beta – to understand the upheaval these changes are imparting across Japan's labor and capital markets – and, importantly, its investible universe. But just to cover a few – such changes are forcing adaptation, higher wages, new investment, new thinking, cost efficiencies, capital reallocation, industry consolidation and pricing power. And critically, these adaptations are increasingly being undertaken by a new generation of decision makers - that post-1970 cohort, shaped not by the era of high post-war growth and the bubble, but by stagnation and globalisation, distrustful of the ways of their parents' generation – and with fundamentally different instincts about capital, risk, talent, and shareholder value.

The alpha opportunities for all this are immense, and they come from understanding that universe intricately enough – at the individual company level – to be able to identify who will win and who will lose. What seems certain is that the universe of Japanese stocks will be unrecognizable at the end of these changes, versus when they began. And THAT is the opportunity.

The final end to 3-decades of deflation and a deflationary mindset - and the transition to accelerating inflation expectations

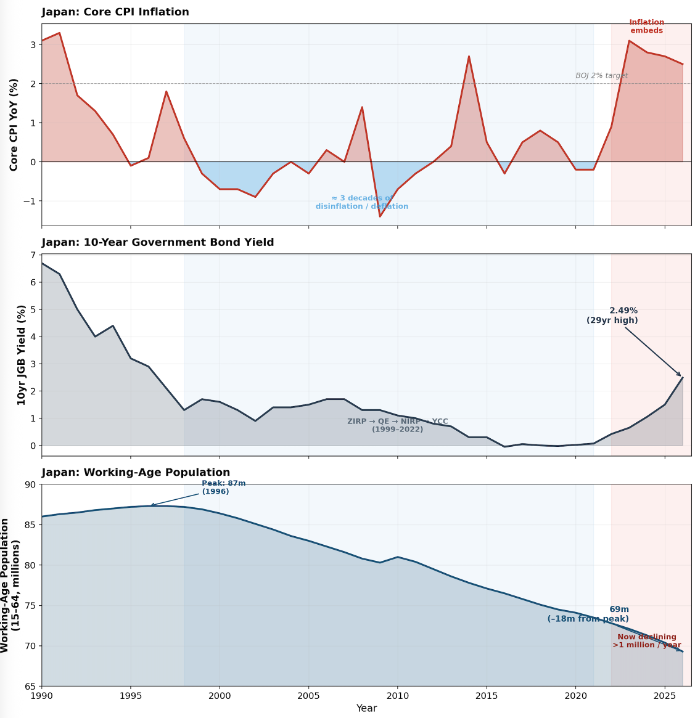

This is the other core change at the heart of the Japan opportunity – and it goes hand-in-hand with the demographics above – and its implications for alpha-generation are equally momentous. It's really only within the last 3 years – after nearly three decades of disinflation, deflation and stagnation, that the stultifying hold of Japan's deflationary trap over the country and its people, has finally broken. For anyone who hasn't lived through it, it is hard to overemphasize the impact of this transition. For an entire generation, prices fell or stagnated; wages too; cash was hoarded; leverage punished; and risk-taking was actively avoided. Japan's corporate and household sectors optimised for a world in which the price level either declined or stood still - forever. That world view is over. Japan's core CPI has been positive for over three years; wage growth is accelerating; and the BOJ has begun carefully normalising – after decades of ZIRP, QE, NIRP and YCC – scared however not to get ahead of the curve. The yield curve is steepening and, for the first time in a generation, embedding genuine risk premia. (I wrote on this rise in the 10 year JGB yield - to a generational-high - last week. This week, it has risen further).

These moves reflect a deep structural regime change, underwritten and amplified by the very demographic pressures described above – and reinforced by global supply-chain reconfiguration and energy-price dynamics. These are the factors that led US Treasury Secretary Scott Bessent to warn last year that; "the Japanese have an inflation problem…"

And it perhaps goes without saying that corporate implications are simply enormous: pricing, inventory, leverage, compensation, and investment decisions all change when prices rise - and when mindsets flip like this. Companies must adjust, and quickly, but the speed and willingness with which individual companies adapt still varies enormously. Many are left like deer in the headlights. Deflationary mindsets persist – usually among the older generation. And like with the demographics above, this staggered adjustment creates huge alpha; if you know each individual company well enough - if you've looked into management's eyes.

Demographics and Inflation are Deeply Intertwined – amplifying the potential Alpha

Moreover, these two core dynamics are not parallel developments that happen to be occurring at the same time. They are causally linked. Demographics help drive the exit from deflation - a shrinking workforce with rising bargaining power pushes wages, which pushes costs, which pushes prices. And inflation, in turn, is accelerating the behavioural consequences of the demographic shift - because an inflationary environment makes the old deflationary playbook (hoard cash, avoid leverage, suppress prices, cling to seniority) not just outdated but actively destructive of value. The companies and leaders that recognise this - and the many that do not - are diverging at speed.

Indeed, we see a cascade of second-order / derivative effects now in play across corporate Japan - each one is a structural phenomenon in its own right, and each with tradeable stark winners and losers. And each one, for the investor who can identify the right and wrong side of the shift at the individual company level, is an alpha opportunity.

Such derivative effects include;

Where demographics and inflation work together – amplifying alpha opportunities

Several of the most consequential shifts sit at the intersection of demographic change and the end of deflation. These offer the richest alpha opportunities of all, because they are driven by two irreversible forces simultaneously - making the divergence between winners and losers wider and more persistent.

Acceleration in M&A. Japan's M&A market is entering a structural growth phase. On the demographic side, tens of thousands of SME founders are ageing out with no successors - creating a pipeline of acquisition targets unprecedented in Japan's post-war history. On the inflation side, activist pressure, governance reform, and the unwinding of cross-shareholdings are creating deal catalysts and removing the cultural barriers that once prevented transactions. The acquirers, the targets, and the companies left behind by consolidation will deliver profoundly different returns. Picking the right side of each transaction is a pure alpha exercise, combining M&A expertise with particular knowledge of individual companies or industries.

Corporate Governance and Shareholder Returns. The TSE reforms - demanding that companies trading below book value articulate credible improvement plans - have been a catalyst, but the deeper shift is cultural and generational. The post-1970 leaders taking charge are more receptive to independent boards, ROE discipline, and genuine accountability. Meanwhile, the inflationary environment makes governance reform urgent rather than optional - because investors will no longer tolerate idle capital when the cost of holding cash is rising. Some companies are transforming at speed. Others are issuing cosmetic compliance documents and changing nothing. The spread in outcomes is enormous.

See the full array of reform initiatives introduced over the last decade – attached to this Insight post; The New Year has started well for Japanese Equities – Now for the next catalyst

The Shift from Risk Aversion to Risk Appetite in Household and Corporate Savings. For a generation, Japanese households kept roughly half of their ¥2,200 trillion in financial assets in cash deposits - earning nothing, risking nothing. That ratio has now fallen below 50% for the first time in eighteen years, with equity holdings surging almost 20% and investment trusts jumping over 21% year-on-year. The catalyst is partly policy - the government's sweeping 2024 NISA reform made the tax-exempt investment programme permanent, raised annual contribution limits, and removed the holding-period cap, generating a surge in new accounts (particularly among under-40s, who now hold over 7 million NISA accounts). But the deeper driver is behavioural; when inflation is positive, holding cash is no longer safe - it is a real loss. This same logic is playing out on corporate balance sheets, where the shift from cash hoarding to capital deployment is accelerating. The changes that this shift will reap upon Japan will be unevenly spread but massive. The companies and financial institutions positioned to capture this multi-trillion-yen migration of savings into risk assets - and those still built for a zero-rate, zero-risk world - will deliver very different returns.

Implications for Japan-based investment strategies – How to extract Alpha.

To be sure, the combination of all the factors cited above have helped the broader Japanese equity indices to more than double over the last three years – and, yes, that rally reflects beta. But within those headline moves, the dispersion between individual stocks has been extraordinary. Indeed, the overall index returns hide the reality of a market bifurcating between companies riding these structural shifts and companies being crushed by them – or just the staggered timing of their adaptation. That dispersion is the alpha. And it is widening, not narrowing, because these structural forces are accelerating.

Moreover, as is obvious, each of the factors cited above are not independent – but rather reinforce each other. A company led by the post-1970 generation of manager is more likely to embrace pricing power, adopt AI, deploy cash, take leverage, and link pay to performance. The winners tend to win across multiple vectors simultaneously. The losers tend to lose across multiple vectors simultaneously. This correlation of outcomes at the company level magnifies the alpha opportunity - and makes bottom-up stock selection not just relevant, but essential – and abnormally profitable.

The rewards for deep expertise and an on-the-ground presence – enhanced Alpha extraction

If the alpha in Japan lies in identifying which companies are genuinely adapting and which are merely performing compliance, then extracting it demands a very particular set of capabilities:

So to quickly sum this all up, while many foreign investors understand that "Japan is Changing" – they may not fully understand that it describes one of the biggest structural stories seen among developed-market equities in a generation. Without that deeper understanding of what is actually going on, it can appear through the lens of traditional portfolio theory, like beta - a broad market phenomenon, a country call, an ETF trade. That view is misguided. The reality is that within each of these structural shifts lies a profound divergence in company-level outcomes, which in turn can come down to whether management gets it or not. That divergence is alpha. You can feel it here everywhere – but you need to be here, on the ground, every day. Come and feel it for yourself. Come say hello when you do.

Charts: Japan's Once-in-a-Generation Structural Shift – in CPI, JGB Yields & Population (But it's what's happening under the hood that's creating the massive opportunity for alpha generation)

.svg)