The heady mix that could finally tip Japan from good inflation to bad inflation

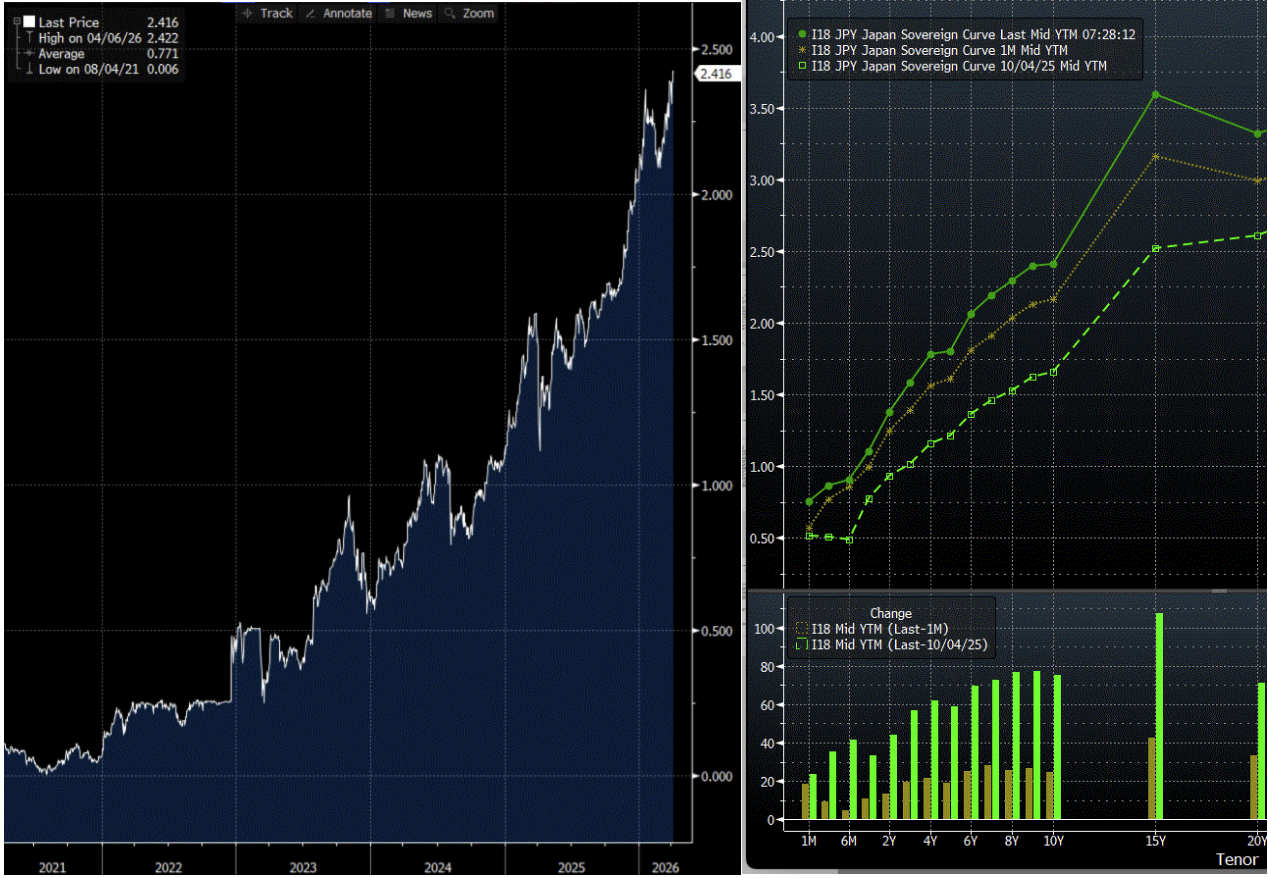

Today, after one of the longest and most contested budget seasons in recent memory, the Diet is set to finally push through the Prime Minister Takaichi’s first full annual budget. In anticipation, the 10-year JGB yield closed its highest level this millennium – at 2.43%. The two facts are not unrelated. And on almost any other day, that alone would be the story.

But it isn’t, because the budget itself is only one piece of what is shaping up to potentially be the most consequential fiscal moment Japan has faced in a generation. The headline figure, a record ¥122.3 trillion does not capture the full picture. Stacked on top of theFY2025 supplementary budget passed in late December (¥18.3 trillion of additional spending sitting inside a ¥21.3 trillion package, of which roughly ¥8.9 trillion went to household cost-of-living relief and ¥6.4 trillion to so-called strategic investment), and bridged through the spring by an ¥8.6 trillion provisional budget - the first stopgap of its kind in eleven years, made necessary when Takaichi’s 23 January dissolution slipped the calendar - the total fiscal envelope under the Takaichi government for the year now sits comfortably above ¥140 trillion. New JGB issuance to fund all of this comes to roughly ¥29.6 trillion in the initial budget alone, with another ¥11.7 trillion of fresh bonds bolted on through the December supplementary, for a combined fresh-debt take of around ¥41 trillion. Gross JGB issuance for FY2026 is planned at over ¥180 trillion. These numbers reveal that Japan is leaning fiscally into the cycle harder than it has at any point outside of the COVID emergency.

It is worth pausing on what that really means, because the structure of this spending matters every bit as much as its size. In her Diet address on 20 February, just after the landslide election victory that gave her an historic mandate to govern, Takaichi was particularly explicit about her economic policy ambitions. The two signature prongs of it were laid out as;

「責任ある積極財政」 — Responsible Proactive Fiscal Policy

「経済構造の転換と成長力の強化」 — Structural Transformation and Strengthened Growth

The catch phrases flatter and obscure the substance. In plainer language, Takaichi promised two things at once: to spend aggressively, and to push the private (household & corporate) sector — still sitting on the world’s largest pile of low-yielding cash and deposits — out of safety and into risk. She has been faithful to both promises since taking office. Her concluding catch-phrase from that 20 February address — 「成長のスイッチを押して、押して、押して、押しまくってまいります」, roughly, “I shall press, and press, and press, and keep pressing the growth switch” — underscored her conviction.

The problem is that – under closer scrutiny - these two prongs sit in uncomfortable tension with each other. Aggressive pro cyclical fiscal expansion, at a moment when underlying inflation in Japan is already running at its highest sustained pace in three decades, requires the bond market to absorb a torrent of new issuance, arguably unnecessarily. The traditional buyer of that issuance — Japanese households and corporates, via the banks, the life insurers, and the postal savings system — is now being actively encouraged by the same government to do exactly the opposite of what it has done for forty years. Save less. Take risk. Diversify out of cash. Out of JGBs. Out of safety.The 「資産運用立国」 framing — i.e., the ambition to make Japan an “asset-management nation”, to push savings into investment — is an explicit policy goal, even while those very same savings are still required togo on quietly funding a debt stock north of 250% of GDP. It is, at the best of times, a risky policy mix. And the BoJ’s Flow of Funds data has already started to reflect the dilemma: corporate net savings, on a rolling twelve-month basis, has roughly halved against the prior year – suggesting that the marginal domestic buyer of duration is getting harder to find. It is exactly the configuration in which a disorderly bear-steepening of the yield curve becomes possible — long-dated yields rising not because grow this firming, but because the marginal buyer has stopped showing up.

That was already the risk in Takaichi’s reflationary policy ambition seven back when she first won her party’s leadership in October last year (as I wrote at the time). It was only reinforced by her landslide election win in February. And then Iran happened.

The war in the Persian Gulf potentially changes everything, and it does so in three distinct but mutually reinforcing ways. Each of them, on its own, pushes the conflicting policy trends further and faster down the road than previously imagined. Together, they potentially dangerously amplify the impact.

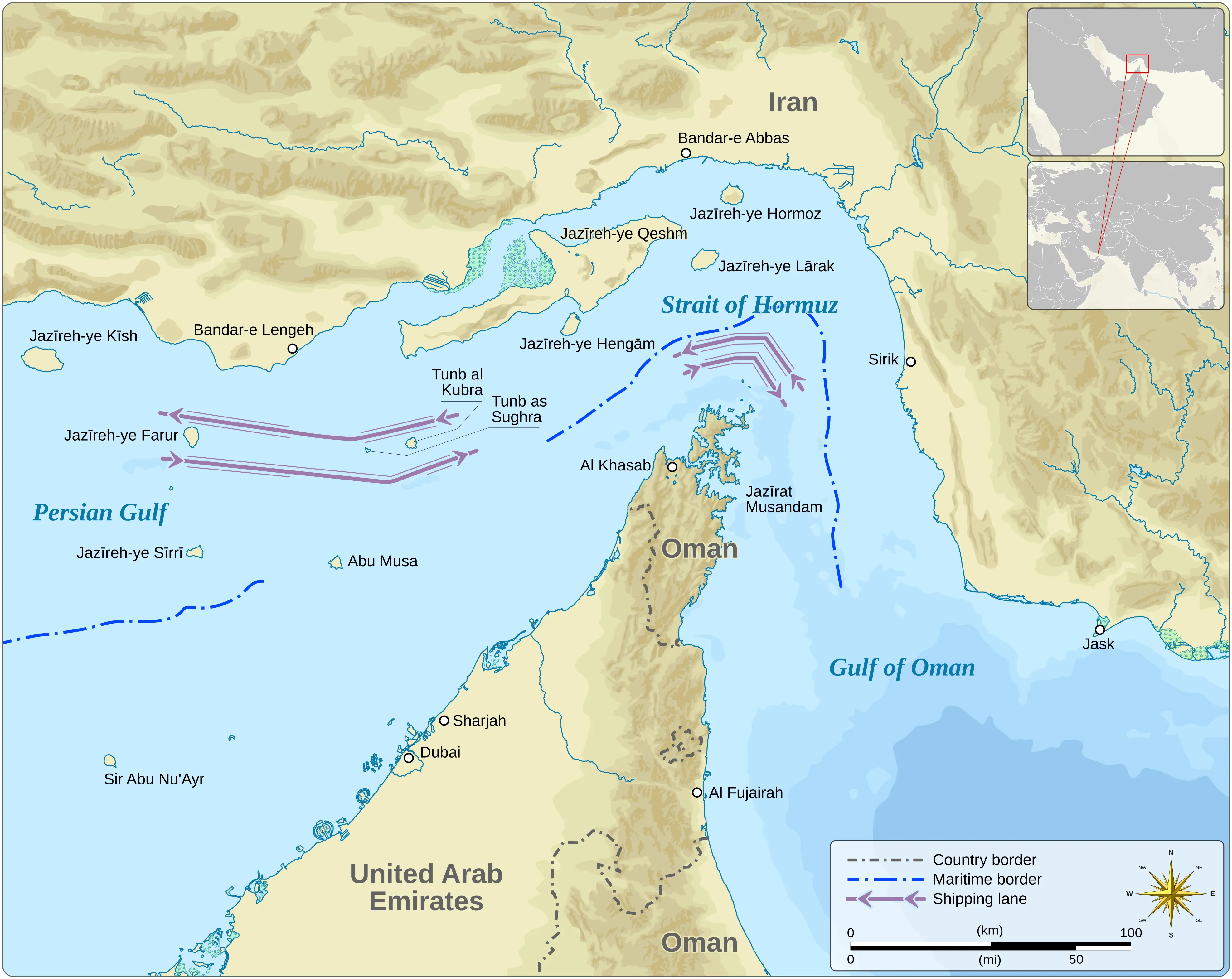

The first is the most obvious and concrete. Brent crude price has moved from the high-$70s in early March to north of $95 in the days since the strikes, and the curve is now pricing a meaningful probability of a sustained spike above $110 should the Strait of Hormuz come under genuine and prolonged disruption. Japan imports roughly 95% of its crude from the Middle East, and a substantial share - by most reasonable estimates around 70% of its seaborne barrels - transits Hormuz. There is no economy in the OECD more exposed to aHormuz shock than Japan’s. The translation into headline inflation, into the trade balance, and through the trade balance into the yen, is mechanical and it is quick. Unsurprisingly, this has further weakened the yen, which in turn feeds back into imported inflation.

The second is political and rhetorical, and it is arguably the more important of the three. National security, quite suddenly, is no longer a subject for political debate. Takaichi’s defence spending in the FY2026 initial budget will be the largest single-year build-out in postwar Japanese history - and that figure was always going to draw political pushback. But the Iran shock removes, in a single stroke, the political space in which Takaichi’s opponents had been trying to constrain the defence build-out. The vocal LDP back-benchers and opposition voices that had been pushing back against the size of the supplementary, the scope of the strategic spending lines, and the optics of running such a pro cyclical fiscal stance into accelerating inflation — have turned quiet. National security is the trump card in any Japanese fiscal debate, and Takaichi has just been handed it (a point made in this recentFT article).

The third pressure is the household one, and it is where the policy becomes properly self-reinforcing. Takaichi promised, as a core electoral pledge, to lower the cost of living — and specifically to do something about gasoline prices. What is not always understood outside Japan is that pump prices here are already being held down materially by existing METI subsidies; the support rate is presently running at over ¥50 per litre, funded out of an ¥800 billion reserve, and is the only reason retail gasoline is sitting at roughly ¥160-170a litre rather than the ¥220 or so it would otherwise reach — fully 30% higher than where the consumer actually sees it today.

The arithmetic of preventing a politically catastrophic spike at the pump on top of the Hormuz move means that the subsidy envelope is about to get materially larger. That is more fiscal stimulus, more issuance, and, critically, stimulus delivered straight into the pocket of the consumer at the precise moment that headline inflation is being pushed up by the same external shock the subsidies are designed to mask. It is, in textbook terms, exactly the wrong policy at exactly the wrong time. It is also, in political terms, the only policy.

So put the three together. A government already committed to a record fiscal expansion, with over ¥40 trillion of fresh debt to place in a single fiscal year. A private (household & corporate) sector being actively pushed out of the very savings instruments that comfortably fund that expansion. And now an exogenous shock that forces the same government to spend more on defense, more on subsidies, more on cushioning households — while simultaneously handing it the political cover of a national security crisis with which to silence those voices that had been counselling restraint. This is the heady mix the Takaichi platform always promised. But the Iran war may now add the lighter fluid.

Which brings us back to these recent moves in JGB yields. In light of the above, 2.4% on the 10 year arguably does not look like a peak. Japan’s emergence out of nearly three decades of deflation and disinflation has, until now, been remarkably gradual, remarkably ordered, and remarkably well-managed. Markets have, on balance, given the BoJ and the MoF the benefit of the doubt that this would continue. As I have argued now repeatedly, the underlying changes already underway in Japan — the visible shift in cash use, the genuine pickup in capex, the willingness of corporates to raise prices and to raise wages — are bigger, faster, and more durable than the official commentary tends to admit. What the budget and the Iran war jointly raise is the prospect that the orderly part of the transition may now be behind us. The pivot from gradual to sharp could come not because the BoJ has lost control, but because the fiscal authority has given up its own constraints.

The risk seems real now that the move in long-dated yields continues. One hopes, of course, it does not turn disorderly. However, if the circumstances laid out above don’t change soon, what else will stop it? The BOJ?

Acceleration in JGBs yield steepening under Takaichi

.svg)